Institute of Chartered Accountants of Pakistan

| انسٹی ٹیوٹ اف چارٹرڈ اکاونٹینٹ اف پاکستان | |

| |

| Abbreviation | ICAP |

|---|---|

| Formation | July 1, 1961 |

| Legal status | Body corporate established under The Chartered Accountants Ordinance, 1961 that was promulgated by the President of Pakistan |

| Objective | Regulate the auditing and accounting profession in Pakistan |

| Headquarters | Karachi |

| Membership | 8,818 as of October 2016 |

| Students | >35,000 |

| Member's designations | ACA (Associate) and FCA (Fellow) |

| Official languages | English, Urdu |

| President | Nadeem Yousuf Adil |

| Vice President (North) | Nazeer Ahmad Ch |

| Vice President (South) | Khalil Ullah Sh |

| Governing body | Council |

| IFAC member since | October 7, 1977 |

| Offices | Karachi, Lahore, Islamabad, Peshawar, Multan, Faisalabad, Gujranwala, Sukkur, Quetta and Mirpur AJK |

| Website |

www |

Institute of Chartered Accountants of Pakistan (ICAP) is a professional accountancy body in Pakistan. As of July 2010, it had 7,200 members working in and outside Pakistan.[1] The institute was established on July 1, 1961 to regulate the profession of accountancy in Pakistan. It is a statutory autonomous body established under the Chartered Accountants Ordinance 1961. With the significant growth in the profession, the CA Ordinance and Bye-Laws were revised in 1983.

In view of globalization of the accountancy profession, the Institute is in the process of updating the Ordinance and Bye-Laws once again.

The course of ICAP involves a blend of theoretical education and practical training which run concurrently for a period of 3.5 years and equips a student with knowledge, ability, skills and other qualities required of a professional accountant.

The head office of the institute is in Clifton, Karachi where it has its own premises. The institute also has regional offices at Lahore, Islamabad, Peshawar, Multan, Gujranwala, Sukkur, Quetta, Mirpur (AJK) and Faisalabad.[2]

History

1850–1881

In Indian subcontinent there were a few British firms of accountants, but they were so busy that their services were not available to the general public. The public companies used to appoint a European auditor for safeguarding the interests of the European shareholders, and an Indian auditor with the objectives of safeguarding the interests of the Indian shareholders. The audit of financial statements were conducted under the Companies Act 1850.[3]

1882–1913

Then the Companies Act of 1885 was passed. Regulations 83–94 of Table A contained in the First Schedule provided for the audit of accounts of the companies adopting that table and for the appointment, remuneration and duties of the auditors. In those times, it was not necessary for an auditor to be a qualified accountant. Companies used to employ lawyers as their auditors.[3]

1913–1932

On 1 April 1914, the Companies Act, 1913 was passed and it was necessitated that every auditor of a public limited company must be a certified auditor by the government. The provincial governments were empowered to grant auditors' certificates but, at the same time, the central government also reserved the right to recognise members of certain professional bodies as qualified auditors without obtaining Auditor's Certificate from the government. Consequently, the members of the English, Scottish and Irish Institutes of Chartered Accountants and the English Society of Incorporated Accountants and Auditors were recognised as qualified auditors.

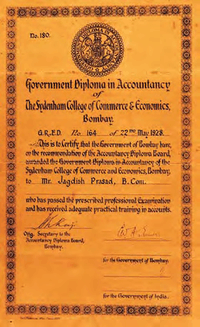

At that time there was no provision of any kind for the training and examination of the accountants. Government of Bombay was the first provincial government to take a constructive step in the direction of organising the profession. In 1918, it instituted the Government Diploma in Accountancy called GDA and made regulations for the examination and training of those who wanted to obtain that Diploma and certificate to practise.

An Accountancy Board was set up by the Government and was attached to the Sydenham College of Commerce and Economics, Bombay. This functioned till 1932. The Board was required to register apprenticeships and conduct the required examinations. The successful candidates were granted the GDA Diploma and they could practise if they had previously received training as apprentices with a practising accountant. The Accountancy Board was also required to advise the Government on all matters relating to accountancy and the Government.[3]

1932–1947

In 1932, the Government framed rules under Section 144 of the companies Act, 1913, called Auditors' Certificates Rules, 1932. The objectives of the rules, broadly, were to register apprenticeships, to conduct examinations, and to control and regulate the profession of auditing. The accountancy profession was then being supervised and controlled by the Ministry of Commerce of the Central Government. With a view to helping the Government in discharging the necessary responsibilities in respect of the accountancy profession, Indian Accountancy Board was established. The Board consisted of officials and practising accountants nominated by the Government. Later, in 1939, appointment of a majority of the members on the Board was made on the elective principle. The Board was only an advisory body. The Auditors' Certificates Rules, 1932, required the passing of two examinations – Registered Accountants first and final. It further laid down the tenure of the prescribed training which was required to be completed during the period of apprenticeship. Provisions meant to regulate and control the profession were also contained therein.[3]

1947–1984

After independence, Pakistan adopted the Auditors' Certificates Rules 1932 with certain amendments in 1950, and thus the auditing profession was administered under the Auditors' Certificates Rules, 1950. The Rules of 1950 were generally based on the old rules with some amendments incorporated therein. A person who passed the Registered Accountants first and final examinations and who satisfied the Ministry of Commerce, Central Government of Pakistan that he had completed the prescribed practical training could have his name placed on the register maintained by the said Ministry and was entitled to use the designation 'Registered Accountant' (RA). The Companies Act, 1913, as adapted by Pakistan allowed only a Registered Accountant to act as the auditor of a public limited company, although his services could also be utilised for the audit of private companies, partnership, etc.

In 1952, the Registered Accountants formed a private body known as 'Pakistan Institute of Accountants' with the object of looking after their own interest and taking up with the Ministry of Commerce, Government of Pakistan, matters affecting the accountancy profession.

In June 1959 the Department of Accountancy was established in the Ministry of Commerce with a Controller of Accountancy to deal with the profession instead of a Section Officer.

During this period, an advisory body called the 'Council of Accountancy' was set up under Auditors' Certificates Rules, 1950 and recommended the establishment of the Institute of Chartered Accountants in Pakistan. The Government accepted the recommendations and the Department of Accountancy assisted by the officials of the Institute and a number of its members prepared the Draft Ordinance to be passed.

The Chartered Accountants Ordinance, 1961, received the assent of the President of Pakistan, Field Marshal General Ayub Khan on March 3, 1961 and was published in Part 1 of the Extraordinary Gazette of Pakistan on March 10, 1961. The Institute of Chartered Accountants of Pakistan came into being on July 1, 1961. A draft of the Chartered Accountants Bye-Laws was also prepared and published for inviting public comments. The amended version called the Chartered Accountants Bye-Laws, 1961 was published in the Part 1 of the Extraordinary Gazette of Pakistan on July 1, 1961 and was enforced as on that date. As of that date the Department of Accountancy and the Pakistan Institute of Accountants having served a very useful purpose for a long time were finally liquidated.

The Chartered Accountants Bye-Laws provided for the formation of regional committees to look after the interests of their members. The members are divided into two classes – namely, Associate Chartered Accountants (ACA) and Fellow Chartered Accountants (FCA).[3]

1984-till now

In December 1984, the Companies Act, 1913 was replaced by the Companies Ordinance, 1984 with an order by the President of Pakistan General Zia-ul-haq. With this Ordinance, it was also necessitated for the manufacturing concern to prepare and maintain cost accounting records and to arrange cost audit on annual basis by a Chartered Accountant or a Cost and Management Accountant. It also lays down the requirements for the preparation of financial statements of unlisted companies. For listed companies the above Ordinance also made mandatory the National Accounting Standards (NAS) and other standards to be strictly followed while preparing financial statements.

Keeping in view the convergence, undergone by the major economies of the world such as United States of America, China and Canada, of the International Financial Reporting Standards with respective local GAAP, the demand for IFRS specialists is increasing. The Institute of Chartered Accountants of Pakistan (ICAP) has introduced a diploma in IFRS to prepare the candidates to avail such opportunities.

Mission statement

The profession of Chartered Accountants in Pakistan should be the benchmark of professional excellence upholding the principles of integrity, transparency and accountability.

"To achieve excellence in professional competence, add value to businesses and economy, safeguard public interest; ensure ethical practices and good corporate governance while recognizing the needs of globalization."

Presidents and members

Past Presidents till present are as follow;

| Year | Past Presidents | Organization |

|---|---|---|

| 1961–1962 | S. Osman Ali | Ministry of Finance (Pakistan) |

| 1962–1963 | M. Ahmad | Ministry of Finance (Pakistan) |

| 1963–1966 | Waqas Aslam | Ministry of Finance (Pakistan) |

| 1966–1969 | Vaqar Ahmed | Ministry of Finance (Pakistan) |

| 1969–1970 | A. Rab | Ministry of Finance (Pakistan) |

| 1970–1972 | V. A. Jafarey | Ministry of Finance (Pakistan) |

| 1972–1973 | M. Yakub | Ministry of Finance (Pakistan) |

| 1973–1975 | Ejaz Ahmed Naik | Ministry of Finance (Pakistan) |

| 1975–1978 | Abdur Raouf Shaikh | Ministry of Finance (Pakistan) |

| 1979 | Aftab Ahmed Khan | Ministry of Finance (Pakistan) |

| 1979–1983 | H. U. Beg | Ministry of Finance (Pakistan) |

| 1983–1986 | Irtiza Husain | Ministry of Finance (Pakistan) |

| 1986–1988 | Ebrahim Dahodwala | BDO International Pakistan |

| 1988–1989 | M. Afzal Munif | BKR International Pakistan |

| 1989–1991 | Ebrahim Sidat | Ernst & Young Pakistan |

| 1991–1992 | Abdul Hameed Chaudhri | Hameed Chaudhri & Company |

| 1992–1993 | Khalid Rafi | PricewaterhouseCoopers Pakistan |

| 1993–1994 | Muhammad Yousuf Adil | Deloitte Pakistan |

| 1994–1996 | Syed Masoud Ali Naqvi | KPMG Pakistan |

| 1996–1997 | Sajjad Ahmad | PricewaterhouseCoopers Pakistan |

| 1997–1998 | Ahmad Dawood Patel | Ernst & Young Pakistan |

| 1998–1999 | Najam I. Chaudhri | PricewaterhouseCoopers Pakistan |

| 1999–2000 | Shaukat Amin Shah | ICAP Members Exclusive |

| 2000–2001 | Pir Mohammad A. Kaliya | First Paramount Modaraba |

| 2001–2002 | A. Husain A. Basrai | KPMG Pakistan |

| 2002–2003 | Khaliq-ur-Rahman | Grant Thornton Pakistan |

| 2003–2004 | Mujahid Eshai | CHARTAC BUSINESS SERVICES (PVT) LTD |

| 2004–2005 | Zafar Iqbal Sobani` | Hub Power Company |

| 2005–2006 | Syed Mohammad Shabbar Zaidi | PricewaterhouseCoopers Pakistan |

| 2006–2007 | Nasimuddin Hyder | Ernst & Young Pakistan |

| 2007–2008 | Imran Afzal | Grant Thornton Pakistan |

| 2008–2009 | Syed Asad Ali Shah | Deloitte Pakistan |

| 2009–2010 | Abdul Rahim Suriya | A.R.Suriya& Co, Chartered Accountants |

| 2010-2011 | Shaikh Saqib Masood | KPMG Pakistan |

| 2011-2012 | Rashid Rahman Mir | Rusell Brad Ford Pakistan |

| 2012-2013 | Ahmad Saeed | Mazars Consulting |

| 2013-2014 | Naeem Akhtar Sheikh | HASSAN NAEEM & CO |

| 2014-2015 | Yacoob Suttar | ASIA PETROLEUM |

| 2015-2016 | Hafiz Mohammad Yousaf | NCBMS Consulting |

| 2016-2017 | Nadeem Yousuf Adil | Deloitte Pakistan |

The member statistics till 2010 are as follows;

| Area of occupation | North region | South region | Total |

|---|---|---|---|

| Commerce and Industry | 1,179 | 983 | 2,161 |

| Corporation | 9 | 4 | 13 |

| Education | 37 | 38 | 75 |

| Financial Institution / Banks | 297 | 90 | 388 |

| Government | 24 | 21 | 45 |

| Employed in Practice | 237 | 182 | 419 |

| Non-Practice (Overseas) | 779 | 353 | 1,132 |

| Public-Practice (Overseas) | 16 | 3 | 19 |

| Public-Practice (Domestic) | 290 | 358 | 648 |

| Others (Overseas) | 9 | 1 | 10 |

| Others (Domestic) | 81 | 21 | 102 |

| Life Member | 43 | 23 | 66 |

Five year Statistical Data of Members

| Year | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| Members | 3,864 | 4,110 | 4,243 | 4,709 | 5,078 | 5,305 | 5,589 | 6,082 | 6,400 | 6,720 | 7,141 |

Student

The Institute provides students the login tab on its website.[6] The Institute committed to regulate the education, training and examination of its students in order to ensure that a newly qualified Chartered Accountant can continue to be confidently regarded as:

- Having a sound grounding in the major subject of accountancy, business, finance and management which can be further developed by continuing education and which can be drawn on for a professional lifetime;

- Being fully equipped with the professional attitudes expected of a member of the Institute;

- Being ready to undertake work, demanding qualities and skills expected of a chartered accountant and being able, with suitable induction, speedily to acquire any additional accountancy skills required for particular task in public practice, industry, commerce or else where.

From 1994 a Pre-entry Proficiency Test (PPT) was introduced to determine the suitability of candidates before being registered as Trainee Students/Full Time Students. PPT was mandatory for all entrants except those who were exempt from PPT but later when new policy was introduced in 2014, it was completely excluded from the course.

Publications

The publications of the Institute are:

- Coffee Table Book

- Newsletter

- The Pakistan Accountant

- MIES

- Technical E-Newsletter

The Pakistan Accountant is the professional flagship publication of the Institute. It is intended to serve as a forum for disseminating information on auditing and accounting practices, business and finance, and topics of current national and international interest.

The Newsletter is designed to provide a heads-up on important Institute events and activities. The Pakistan Accountant and the Newsletter have received a makeover this past year to boost the Institute’s professional image, and to serve as a channel for staying in touch with our most valuable assets – our members and students.

Through the Members Information & Education Series (MIES) the Institute hopes to promote the integration of best practices and sound judgment among members.

These publications form the body of literature that fosters the Institute’s policy of promoting education and research.[7]

International association

The ICAP is a member of International Federation of Accountants (IFAC), International Accounting Standards Board (IASB), Confederation of Asian and Pacific Accountants (CAPA) and South Asian Federation of Accountants (SAFA). ICAP was awarded associate membership by Chartered Accountants Worldwide (CAW), making it the second professional body to be admitted to the organisation since its launch in February 2013.[8]

See also

- Association of Chartered Certified Accountants

- International Federation of Accountants

- Institute of Cost and Management Accountants of Pakistan

- Pakistan Institute of Public Finance Accountants

- Securities and Exchange Commission of Pakistan

Notes

- ↑ Archived June 21, 2008, at the Wayback Machine.

- ↑ "The Institute of Chartered Accountants of Pakistan » Communication with Institute". www.icap.org.pk. Retrieved 2016-03-17.

- 1 2 3 4 5 6 Saeed, Prof. Dr. Khawaja Amjad, Auditing: Principles & Procedures, Lahore: Institute of Business Management, 1993 pages 18–22.

- ↑ http://www.icap.org.pk/icap/our-vision-our-mission/

- ↑ "Symbolising Growth :Annual Report 2013" (PDF). Icap.org.pk. Retrieved 2015-03-10.

- ↑ http://www.icap.org.pk/my-student/

- ↑ http://www.icap.org.pk/icap/publications/

- ↑ http://economia.icaew.com/news/february-2016/icap-joins-chartered-accountants-worldwide

References

- Saeed, Prof. Dr. Khawaja Amjad (1993), Auditing: Principles and Procedures, Lahore: Institute of Business Management.

- ICAP Coffee Table Book, A journey through time, And it can be viewed using this link, http://www.icap.org.pk/wp-content/uploads/CoffeeTable/CTB/index.html#p=14

External links

- Official homepage

- Firms having satisfactory QCR Rating in Pakistan

- Pakistan Accountancy Forum Official Website

- IFACnet – A KnowledgeNet for Accountants in Business

| Asia | |

|---|---|

| Africa | |

| Europe | |

| North America & Caribbean | |

| Oceania | |